![]()

IIA-CIA-Part2 Dumps PDF - IIA-CIA-Part2 Real Exam Questions Answers

Get Started: IIA-CIA-Part2 Exam [2024] Dumps IIA PDF Questions

IIA-CIA-Part2 (Practice of Internal Auditing) Certification Exam is one of the most respected certifications in the field of internal auditing. It is offered by the Institute of Internal Auditors (IIA), which is the global leader in the internal audit profession. Practice of Internal Auditing certification is designed to assess the knowledge and skills of internal auditors in the practice of internal auditing. It is a valuable credential for individuals who want to demonstrate their competence in this field.

NEW QUESTION # 55

As part of an operational audit of the shipping department, an auditor selected a sample of 45 daily shipping logs from the department's files. On 44 of the days, the log contained a sufficient number of shipments to meet the department's daily quota. Based on this test, the auditor concluded that the shipping department was effective at meeting its quotas. Which of the following is true about the auditor's conclusion?

- A. The shipping department is effective in meeting its responsibilities.

- B. None of the above.

- C. The number of items selected for testing is inadequate to justify the conclusion.

- D. This conclusion would negate any need to perform tests of efficiency.

Answer: B

Explanation:

Section: Volume A

NEW QUESTION # 56

A film company determined that income level impacts the number of films that people watch per month, as shown by the graph below:

The graph indicates that:

- A. A 20 percent pay increase is likely to increase film viewing by a constant amount regardless of income level.

- B. A richer person always sees more films than a poorer person.

- C. A 20 percent pay increase is more likely to increase film viewing at lower income levels than at higher income levels.

- D. The number of films seen per month is a linear function of income level.

Answer: C

NEW QUESTION # 57

A staff auditor, nearly finished with an audit engagement, discovers that the director of marketing has a gambling habit. The gambling issue is not directly related to the existing engagement and there is pressure to complete the current engagement. The auditor notes the problem and forwards the information to the chief audit executive but performs no further follow-up. The auditor's actions would:

I. Be in violation of the IIA Code of Ethics for withholding meaningful information.

II. Be in violation of the Standards because the auditor did not properly follow up on a red flag that might indicate the existence of fraud.

III. Not be in violation of either the IIA Code of Ethics or Standards.

- A. II only

- B. I and II only

- C. I only

- D. III only

Answer: D

Explanation:

Section: Volume C

NEW QUESTION # 58

Many questionnaires are made up of a series of different questions that use the same response categories (for example: strongly agree, agree, neither, disagree, strongly disagree). Some designs will have different groups of respondents answer alternate versions of the questionnaire that present the questions in different orders and reverse the orientation of the endpoints of the scale (for example: agree on the right and disagree on the left).

The purpose of such questionnaire variations is to:

- A. Eliminate intentional misrepresentations.

- B. Reduce the effects of pattern response tendencies.

- C. Test whether respondents are reading the questionnaire.

- D. Make it possible to get information about more than one population parameter using the same questions.

Answer: B

Explanation:

Section: Volume A

Explanation

NEW QUESTION # 59

When internal auditors provide consulting services, the scope of the engagement is primarily determined by:

- A. The internal audit activity's charter.

- B. The engagement client.

- C. Internal auditing standards.

- D. The audit engagement team.

Answer: B

NEW QUESTION # 60

An internal auditor is planning to audit the organization's payroll function, which was recently outsourced. Which of the following is the most appropriate first step for the auditor?

- A. Revise the scope of the audit engagement

- B. Review management's organ nationwide risk assessment

- C. Understand the objectives and strategies of the new arrangement

- D. Form objectives for the audit engagement

Answer: C

Explanation:

When planning to audit an outsourced function, the most appropriate first step for an internal auditor is to understand the objectives and strategies of the new arrangement. This step is crucial because it sets the foundation for the entire audit process. By understanding the objectives and strategies, the auditor gains insights into the rationale behind the outsourcing decision, the expected outcomes, and how these align with the organization's overall goals. This understanding helps in identifying key risks, establishing relevant audit criteria, and tailoring the audit scope and procedures accordingly. Without this initial step, the auditor may miss critical aspects of the outsourced arrangement, leading to an incomplete or ineffective audit.

Reference:

Institute of Internal Auditors (IIA) Practice Guide: "Auditing Outsourced Activities" COSO Enterprise Risk Management Framework

NEW QUESTION # 61

Which of the following situations would best support the decision of a chief audit executive (CAE) to defer follow-up activity at a branch office until the next audit engagement?

- A. Branch office management states that correction of the audit issue may take longer than expected.

- B. The CAE and management agree that the corrective action taken to date is sufficient.

- C. On-site follow-up of a remote branch may not be feasible due to travel costs.

- D. An audit of the branch office is routinely scheduled every three years.

Answer: B

NEW QUESTION # 62

Which of the following would constitute a violation of the IIA Code of Ethics?

- A. An internal auditor has accepted an assignment to audit the warehousing function six months from now.

The auditor has no expertise in that area but has signed up for courses in warehousing that will be completed before the assignment begins. - B. An internal auditor discovered an internal financial fraud during the year, and the financial statements were adjusted to properly reflect the loss associated with the fraud. The auditor discussed the fraud with the external auditor during the external auditor's review of the working papers detailing the incident.

- C. An internal auditor, who has recently joined the organization, has accepted an assignment to audit the electronics manufacturing division. The auditor previously served as senior auditor for the external audit of that division and has audited many electronics companies during the past two years.

- D. An internal auditor has no ambitions for promotion and has not engaged in training or other professional development activities during the last three years. The auditor's performance assessments indicate consistent quality of work.

Answer: D

NEW QUESTION # 63

The chief audit executive (CAE) of an organization has established an internal audit activity (IAA) quality assessment program. According to IIA guidance, which of the following would be part of this program?

- A. Assessment of the IAA conducted independently of client feedback, and the review of individual audits to determine the quality and timeliness of supervision.

- B. Compliance with a checklist of required audit procedures, and identified areas of improvement reviewed at the end of the year.

- C. Assessment of the IAA conducted independently of client feedback, and identified areas of improvement reviewed at the end of the year.

- D. Compliance with a checklist of required audit procedures, and review of individual audits to determine the quality and timeliness of supervision.

Answer: D

NEW QUESTION # 64

Which of the following would be a red flag that indicates the possibility of inventory fraud?

I.The controller has assumed responsibility for approving all payments to certain vendors.

II.

The controller has continuously delayed installation of a new accounts payable system, despite a corporate directive to implement it.

III.

Sales commissions are not consistent with the organization's increased levels of sales.

IV.

Payments to certain vendors are supported by copies of receiving memos, rather than originals.

- A. I and II only.

- B. II and III only.

- C. I, III, and IV only.

- D. I, II, and IV only.

Answer: D

NEW QUESTION # 65

According to IIA guidance, which of the following factors should the auditor in charge consider when determining the resource requirements for an audit engagement?

- A. The appropriateness and sufficiency of resources and the ability to coordinate with external auditors.

- B. The number, proficiency, experience, and availability of audit staff as well as the ability to coordinate with external auditors.

- C. The appropriateness and sufficiency of resources as well as the nature, complexity, and time constraints of the engagement.

- D. The number, experience, and availability of audit staff as well as the nature, complexity, and time constraints of the engagement.

Answer: C

NEW QUESTION # 66

All of the following tools are employed to control large-scale projects except:

- A. Statistical process control.

- B. Program evaluation and review technique (PERT).

- C. Gantt charts.

- D. Critical path method.

Answer: A

NEW QUESTION # 67

An internal auditor used a risk and control matrix to prepare a work program for testing a software release. During the engagement planning stage, he tested the design of the release procedure as a key control and concluded that the control was not designed well. During the performance stage, he tested the operation of this control and concluded that it was implemented as designed. Which of the following statements is true regarding this scenario?

- A. A risk and control matrix is not appropriate for this type of engagement.

- B. The test of the operating effectiveness of the control should have occurred at the planning stage.

- C. The test of the control design should have occurred at the performance stage.

- D. The test of the operating effectiveness of the control was not necessary.

Answer: D

Explanation:

If a control is found to be poorly designed during the planning stage, testing its operating effectiveness becomes redundant because even a well-implemented but poorly designed control will not achieve its intended objectives. The primary focus should be on redesigning the control to ensure it is effective in mitigating risks. Therefore, the auditor should not have proceeded to test the operational effectiveness of a control that was already deemed poorly designed.

Reference:

The Institute of Internal Auditors (IIA), International Standards for the Professional Practice of Internal Auditing (Standards)

"Auditing: A Risk-Based Approach to Conducting a Quality Audit" by Karla M. Johnstone et al.

NEW QUESTION # 68

Which of the following would be the least desirable criteria against which to judge current operations of an organization's treasury function?

- A. Company policies and procedures delegating authority and assigning responsibilities.

- B. Finance textbook illustrations of generally accepted good treasury function practices.

- C. Codification of best practices of the treasury function in relevant industries.

- D. The operations of the treasury function as documented during the last audit engagement.

Answer: D

Explanation:

Section: Volume C

NEW QUESTION # 69

A retail sales company has discontinued a product that normally sold for $100. During the first month of a sale of the product, a 20 percent discount was given. Later that sale price was reduced by an additional 40 percent.

What was the overall discount from the original selling price?

- A. 52 percent.

- B. 30 percent.

- C. 60 percent.

- D. 48 percent.

Answer: A

NEW QUESTION # 70

If an auditor expects to find numerous discrepancies between recorded values and audited values of sample selections, which sampling technique would be most appropriate?

- A. Discovery sampling.

- B. Difference estimation sampling.

- C. Attributes sampling.

- D. Probability-proportional-to-size sampling.

Answer: B

Explanation:

Section: Volume A

NEW QUESTION # 71

Which of the following will be an appropriate course of action when an auditor disagrees with a client about a well-documented audit finding?

- A. Change the finding so that it is acceptable to the client.

- B. Defer reporting the item and plan to perform more detailed work during the next audit.

- C. Address the issue with senior management and the board for resolution prior to issuing the final report.

- D. Include both the audit finding and the client's position in the audit report.

Answer: D

Explanation:

Section: Volume A

NEW QUESTION # 72

Which of the following audit steps would an internal auditor perform when reviewing cash disbursements to satisfy IIA guidance on due professional care?

- A. The internal auditor reviews the accounts payable manager's petty cash fund and vouchers

- B. The calculated statistical sample size is 50 however the internal auditor believes errors exist so he decides to increase the sample size to 80

- C. The internal auditor traces serial numbers of computer equipment listed on an invoice to the fixed asset inventory

- D. The internal auditor reviews the related invoice purchase order and receiving report for each sample selection

Answer: D

Explanation:

According to IIA guidance on due professional care, internal auditors should perform thorough and adequate steps to verify the accuracy and legitimacy of transactions. When reviewing cash disbursements, it is essential to check the three-way match among the invoice, purchase order, and receiving report. This ensures that the payment is valid, authorized, and that the goods or services were actually received as ordered. This step is crucial in preventing and detecting errors and fraud, thereby ensuring that the audit findings are reliable and accurate.References:

* IIA Standard 1220: Due Professional Care

* IIA Practice Guide: Auditing Accounts Payable and Disbursements

NEW QUESTION # 73

Which of the following is correct with respect to roles within an enterprise-wide risk management process?

1. The board provides oversight to the risk management process.

2. Executive management owns the risk management framework.

3. Senior management is assigned ownership of risks.

4. Internal audit modifies the risk assessment determined by management.

- A. 1 and 2 only

- B. 1, 2, and 3 only

- C. 3 and 4 only

- D. 1, 2, 3, and 4

Answer: B

Explanation:

Section: Volume D

NEW QUESTION # 74

According to IIA guidance, which of the following is true when the internal audit activity is asked to investigate potential ethics violations in a foreign subsidiary?

- A. Local law enforcement should be involved as they are more familiar with the applicable local laws.

- B. Communication of any internal ethics violations to external parties may occur with appropriate safeguards.

- C. Cross-cultural differences should always be handled by the staff of the same cultural background.

- D. Cultural impacts are less critical where the organization practices uniform polices around the globe.

Answer: B

Explanation:

According to IIA guidance, when the internal audit activity investigates potential ethics violations in a foreign subsidiary, communication of any internal ethics violations to external parties may occur, but only with appropriate safeguards. This ensures that sensitive information is protected and that the organization complies with both local and international legal requirements. Cross-cultural differences and local laws must be considered, but the primary focus is on maintaining appropriate safeguards during communication.

References: IIA Practice Guide - Auditing Ethics Programs, IIA Standard 2440 - Disseminating Results

NEW QUESTION # 75

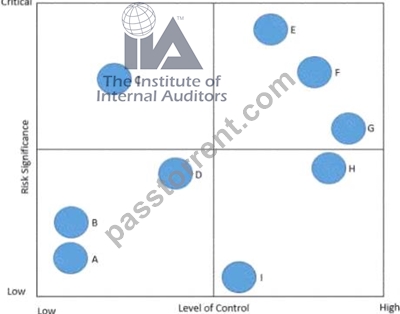

In the following risk control map risks have been categorized based on the level of significance and the associated level of control.

Which of the following statements is true regarding Risk C?

- A. The level of control is appropriate given the level of risk

- B. The level of control is excessive given the level of risk

- C. The level of control is inadequate given the level of risk

- D. There is not enough of information to determine whether the controls are appropriate or not

Answer: C

Explanation:

In the risk control map, Risk C is positioned in the upper left quadrant, indicating it is critical (high risk significance) but with a low level of control.

This suggests that the current controls are insufficient to mitigate the high level of risk associated with Risk C.

For critical risks, a higher level of control is necessary to ensure that the risk is properly managed and mitigated.

References:

* "Internal Auditing: Assurance & Advisory Services" (The Institute of Internal Auditors)

* "Risk Management Framework" (COSO)

NEW QUESTION # 76

During a systems development audit, software developers indicated that all programs were moved from the development environment to the production environment and then tested in the production environment. What should the auditor recommend?

I.Implement a test environment to ensure that testing is not performed in the production environment.

II.

Require developers to move modified programs from the development environment to the test environment and from the test environment to the production environment.

III.

Eliminate access by developers to the production environment.

- A. I and II only.

- B. I and III only.

- C. I only.

- D. III only.

Answer: B

NEW QUESTION # 77

Which of the following procedures would be most helpful in providing additional evidence when an auditor suspects that an unidentified employee is submitting and approving invoices for payment?

- A. Select a sample of receiving reports representative of the period under investigation and trace to approved payment. Note any items not properly processed.

- B. Select a sample of invoices paid during the past month and trace them to appropriate vendor accounts.

- C. Use generalized audit software to identify invoices from vendors with post office box numbers or other unusual features. Select a sample of those invoices and trace to supporting documents such as receiving reports.

- D. Select a sample of payments made during the year and investigate each one for approval.

Answer: C

NEW QUESTION # 78

......

IIA-CIA-Part2 (Practice of Internal Auditing) certification exam is a globally recognized certification offered by the Institute of Internal Auditors (IIA). Practice of Internal Auditing certification is specifically designed for individuals who want to demonstrate their knowledge and skills in the field of internal auditing. IIA-CIA-Part2 exam covers a broad range of topics including risk management, governance, fraud prevention, and internal control.

IIA-CIA-Part2 Premium Exam Engine pdf Download: https://www.passtorrent.com/IIA-CIA-Part2-latest-torrent.html

Verified IIA-CIA-Part2 Bundle Real Exam Dumps PDF: https://drive.google.com/open?id=1kgt1Ulu1VEKeZb4OIEv3bOv0HWHIwfL3